From Chairman's Desk

21 Jun, 2023

Dear Investors,

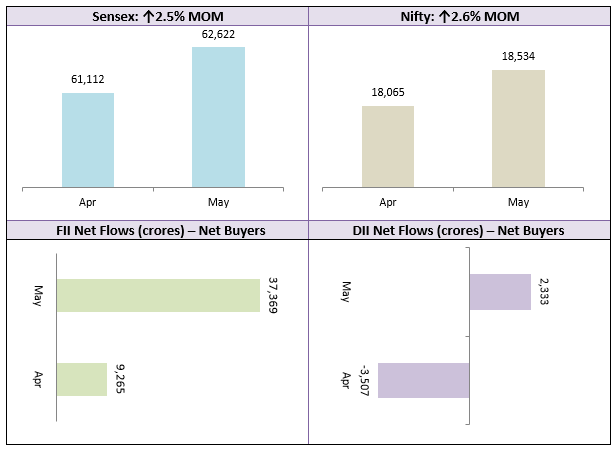

Indian equities continued to gain strength in May. The Sensex and Nifty gained 2.5% to close above 62,500 and 18,500 levels respectively. The resolution of the US Debt Ceiling crisis has provided more confidence to global equities. The meteorological department has forecasted “normal monsoon” this year. This is good news for rural consumption which remained sluggish for many quarters before returning back to growth in Q4 of FY 2023. The IMF is forecasting 6% GDP growth for India in 2023. As per IMF’s forecast, India will be the fastest growing economy among major economies of the world.

India has been the outperformer in the Emerging Markets pack. MSCI India Index (USD) has outperformed the MSCI Emerging Market Index (USD) in the last 3 months. We saw increased buying from FIIs in May. The Nifty is now hear its 52 week high and likely to make fresh highs in the coming months. The broader market outperformed Nifty in May. We are likely to see midcaps and small caps continuing to outperform the Nifty in coming months.

Among industry sectors, automobiles, FMCG and IT were the top performers in May. Banks and financial services, which was the best performing sector in 2022 continued to make solid gains. Q4 corporate earnings of Nifty 50 companies beat the street expectations. However, in view of global economic slowdown the brokerages have revised FY 2023-24 downwards. Overall we expect the market to trend higher in 2023, supported by the US market. Investors should continue to invest in midcaps and small caps through SIPs. You can also take advantage of large corrections by investing in lump sum on dips.

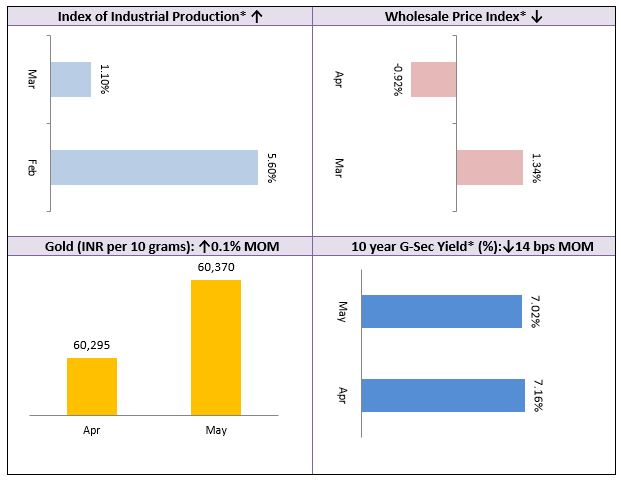

In the commodity markets, Gold is continuing to be firm due to forecast of possible recession in European Union and the US in 2024. We expect gold to remain firm in 2023. Silver will be volatile but may gain strength if the economic data coming out of the US worsens. Crude oil declined further in May due to weaker than expected economic recovery in China. There may be pullback rally from time to time, depending on OPEC production cuts and position of US inventories but we do not expect a major rally in crude in near to medium term.

As far as the debt market is concerned, the 10 year bond yield has eased further, while the 91 day T-Bill yield firmed a bit. As we approach the end of this interest rate cycle duration strategies may be yield higher returns for long term debt investors. Short term investors (1 year or less) can invest in ultra-short duration or money market funds. Medium term investors (2 – 3 years) can invest in corporate bond and Banking & PSU debt funds.

I on behalf of my team, assure you of best service for all your investment needs.

Best Wishes,

Ajoy Agarwal,

(Managing Director)

Get the best investment ideas straight in your inbox!